Skip to content

Skip to content

“Will Singapore property prices drop in 2024? Is it a good time for me to enter the market now, or should I wait for prices to come down?”

It is normal to have these questions given the current high home prices because people are fearful and feeling lost towards the unknown.

No one dares making a move rashly, right?

What if I overpaid? Worse yet, entering the market at the wrong time, there might be a risk of losing money.

Whether you’re a first-time homebuyer or a investor looking for some opinions, you’ve come to the right place. In this article, I will share some data and address these concerns to help you make a more informed decision.

Property Prices Are Sky-Rocketing

Many buyers waiting at bay are witnessing both the prices of HDB and private condos shoot up rapidly over the years without signs of moderation.

Let’s first look at some of the statistics below to see if you can still afford or totally priced out of the market:

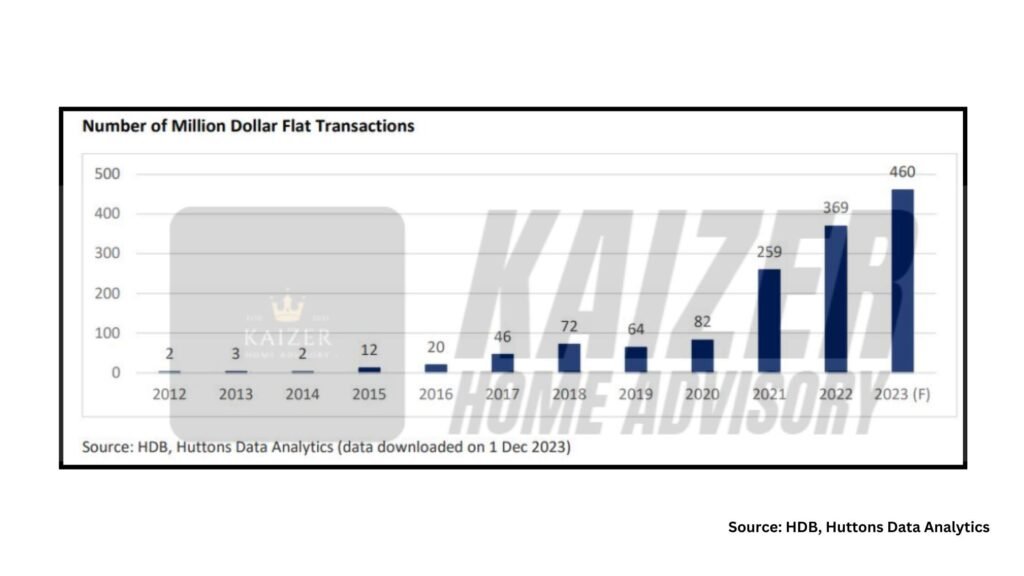

Million dollar HDB Flat

Nowadays we are seeing more and more HDB flats being transacted for over a million dollars.

The graph above illustrates the numbers of million dollar flats are growing every year.

One thing worth noting is that, in the first month alone in 2024, January, a record of 74 HDB flats sold for at least seven figures.

This figure alone is sufficient to cover the entire transaction volume for the year 2020.

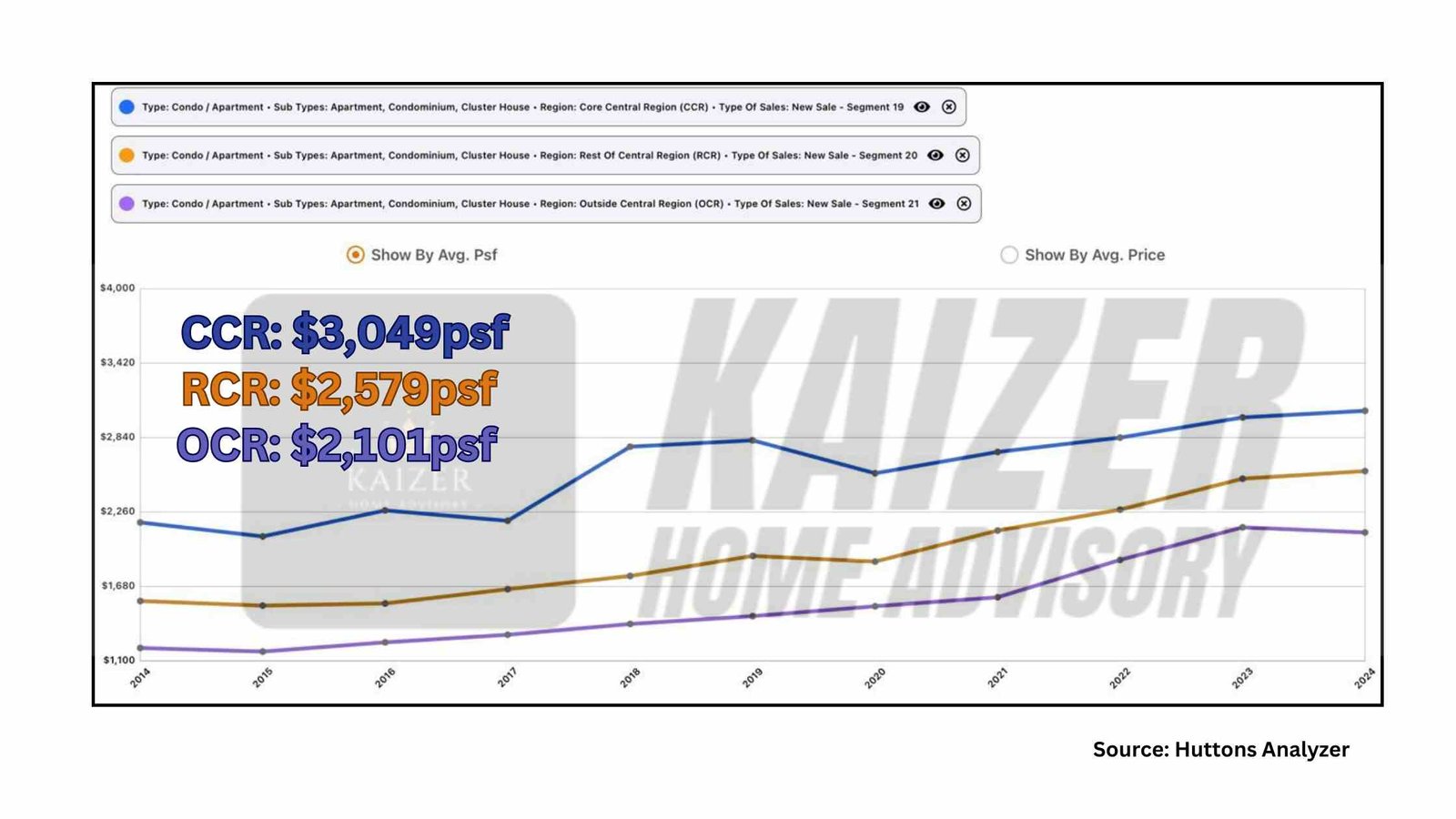

New launch private condo prices

At the same time, the average new private home sales, excluding EC have been seeing new record prices every year.

The OCR private home has always been the top choice for family upgraders trade up HDB flats to private condo considering its relatively attractive price point among the rest.

However, as of Q1 2024, the average price OCR new condo prices have crossed the $2000 mark, setting at $2,101psf.

Meaning to say, if you are looking to buy a brand new family-sized home, similar to your 4 room HDB flat, it will cost you around $2.1m to $2.5m.

Cooling Measures Implemented In 2023

To curb the uncontrolled rise in housing prices, last year the government and banks simultaneously announced and implemented cooling measures.

Many people were shocked. No one knows what substantial impacts would follow.

To play it safe, most buyers adopted a wait-and-see attitude towards the housing market.

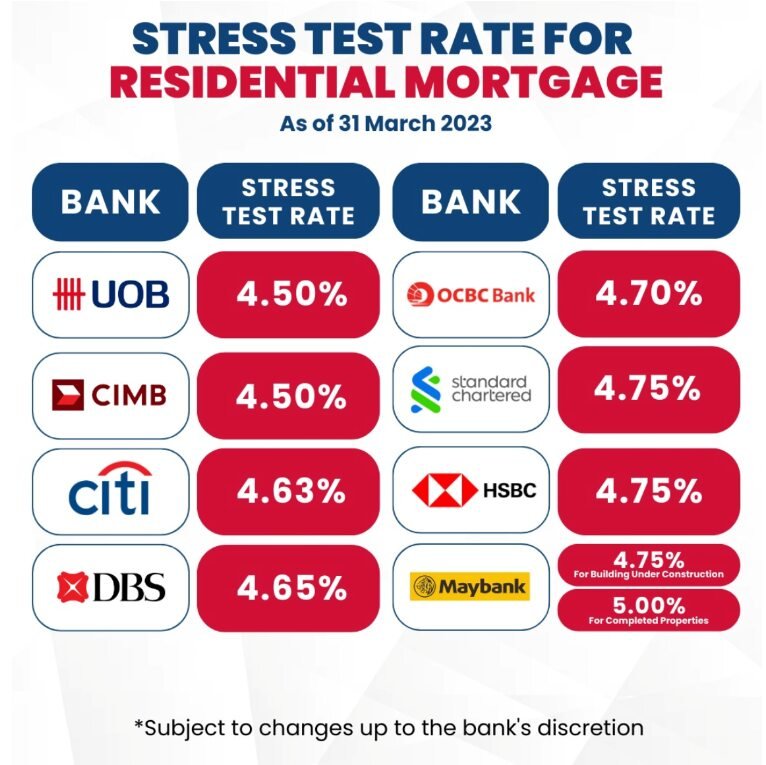

1. Banks increased medium term interest rates

On March 2023, major banks in Singapore adjusted the stress test level to 4.5% – 4.7% range, which is used to calculate the loan eligibility for homebuyers.

Previously it was revised from 3.5% to 4% in September 2022.

To illustrate the impact, check out the table below:

| Loan Tenure | Monthly Installment | 3.5% | 4% | 4.7% |

|---|---|---|---|---|

| 20 | $10,000 | $1.72m | $1.65m | $1.55m |

| 25 | $10,000 | $1.99m | $1.89m | $1.76m |

| 30 | $10,000 | $2.22m | $2.09m | $1.93m |

Assuming at 45 years old, monthly installment at $10k, you were able to get a loan of $1.72m at 3.5% before 2022.

So when the rates were raised to 4.7% in 2023, you can only get a smaller loan size of $1.55m.

The difference of $170,000 can have significant impact on your purchase.

This would translate to more cash top up, sacrificed home size, limited home options.

2. Additional Buyer Stamp Duty (ABSD) Revision

The goal is to deter foreign interest and prioritize Singaporeans to get a family-occupation home. You can read more here.

Clearly, the main target is on foreigners buying residential property, they got hit the hardest with the rate doubled from 30% to 60%.

There was a little fear at first upon the announcement, but homebuyers quickly digested the news and proceeded to snap up their dream home.

As a matter of fact, if you are looking to buy your first home, you are unaffected by the new changes.

3. New BTO classification

As discussed above, the volume of million-dollar flats are increasing, with new record breaking prices after one another.

Is this a good or bad news?

As we all know, HDB flats are meant to be affordable to all Singaporeans. Our government cannot simply watch prices going of out hand.

If prices are left uncontrolled and continue to soar endlessly, then future generations of Singaporeans will not be able to afford public housing.

The new classification for future BTO flats was announced by PM Lee during the National Day Rally 2023 to suppress the “windfall” effect.

Firstly, the standard flats are unaffected at all, same 5 years MOP, no income ceilings for the next buyer for your flat. The only side will be the location being undesirable.

Most million-dollars HDB sold are usually found in prime location near amenities and MRT.

Therefore, starting from second half of 2024, flats located in prime area and near MRT will be labelled as Plus and Prime. They both come with a much longer MOP of 10 years, along with income ceilings of $14k for the future resale buyers.

Another notable term is the 6% subsidy claw back. Meaning a portion of your profit will be recouped by the Government upon the sale of your flat.

So if you belong this category, you will have a tough time commanding high prices in the future alongside these new restrictions handcuffed to your flat.

4 Metrics To Determine Will SIngapore Property Prices Drop

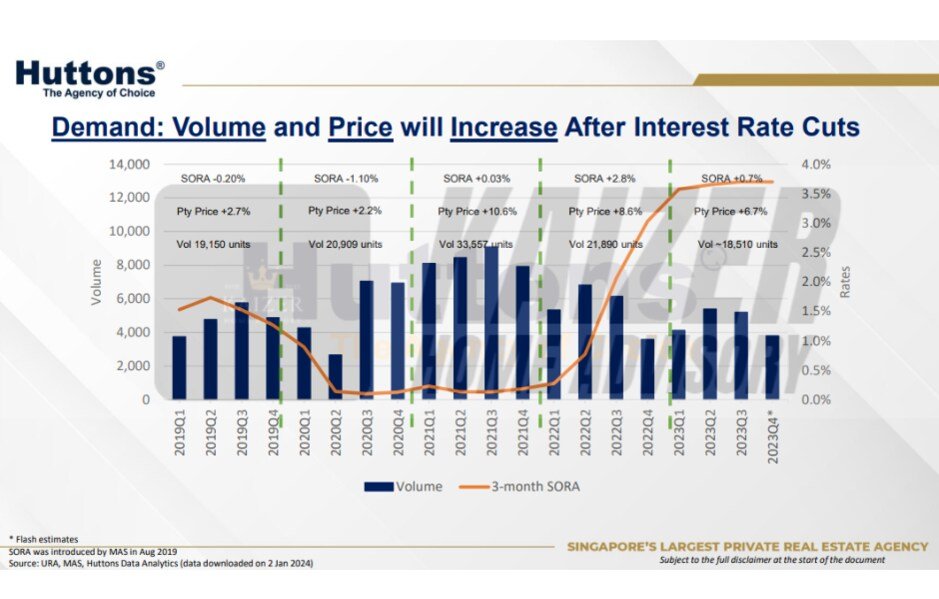

1. Interest rates movement

Throughout history, when interest rates are low, people tend to leverage bank loans along with their own funds to go into investment.

Logically, if you were in the same position, with such low borrowing costs, would you choose to do nothing and keep all your money in a savings account? Or would you take advantage of this to invest into new assets?

Conversely, when interest rates are high, the cost of loans suddenly doubles, many people will find it hard to shoulder. Not to mention large companies and businesses that rely on leverage to maintain normal operations.

”Be fearful when others are greedy, be greedy when others are fearful.” – Warren Buffet

What is the quote trying to tell us?

Taking Singapore’s 2024 property market as an example, with current high interest rates, buying a home now means bearing higher monthly repayments. Thus, many buyers are taking a wait-and-see approach, leading to a decline in overall transaction volume.

What would happen when interest rates drop as anticipated, and borrowing becomes cheaper?

At that point, all the hunger buyers will swarm into the market at the same time.

We all know that when demand rises, prices also increase.

Bringing the focus back to you: Do you think it’s more rational and safer to enter the market when it’s quiet and prices are relatively stable, or when prices are soaring and everyone is rushing in?

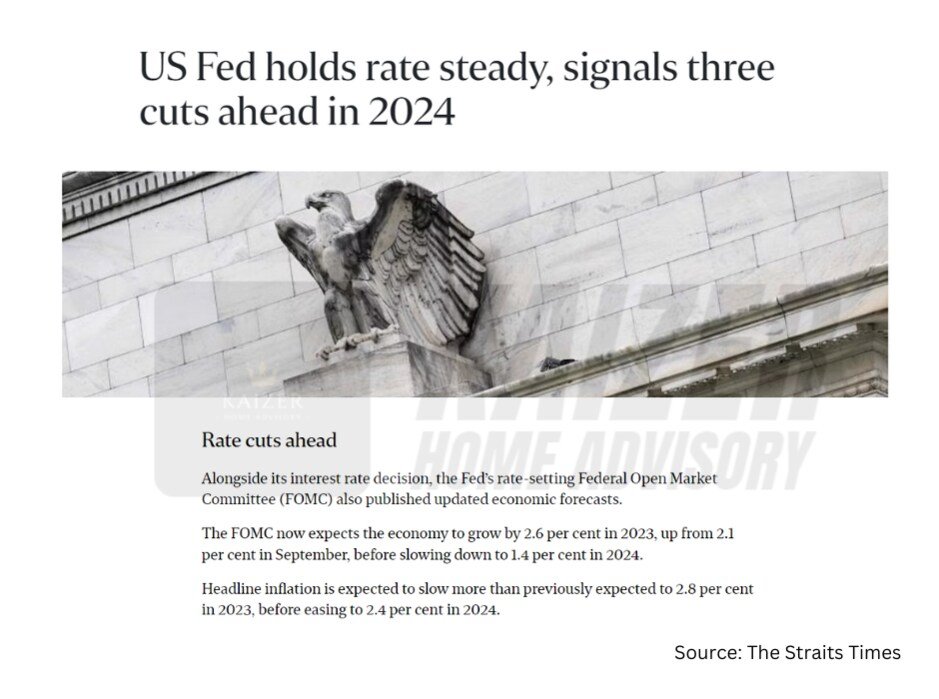

2. Singapore economy growth

Singapore’s economy post-covid was like a thunderstorm, looming and dark. Things may seem a little clear now, though economists warn we are not fully out of the water yet.

That’s because even if the economy and inflation begin to improve, current prices are unlikely to return to their previous levels. Moreover, the war in Europe and the Middle East has not ended, keeping the overall situation tense.

Nevertheless, according to experts, looking at the economic outlook for 2024, it is predicted that economic growth will rapidly recover, with inflation and interest rates coming down in phases, leading to a brighter future.

When the economy improves and people tend gain more confidence in the market, their willingness to invest will increase too.

Imagine, in a bright economic outlook, will Singapore property prices drop? Or will they rise along with the tides?

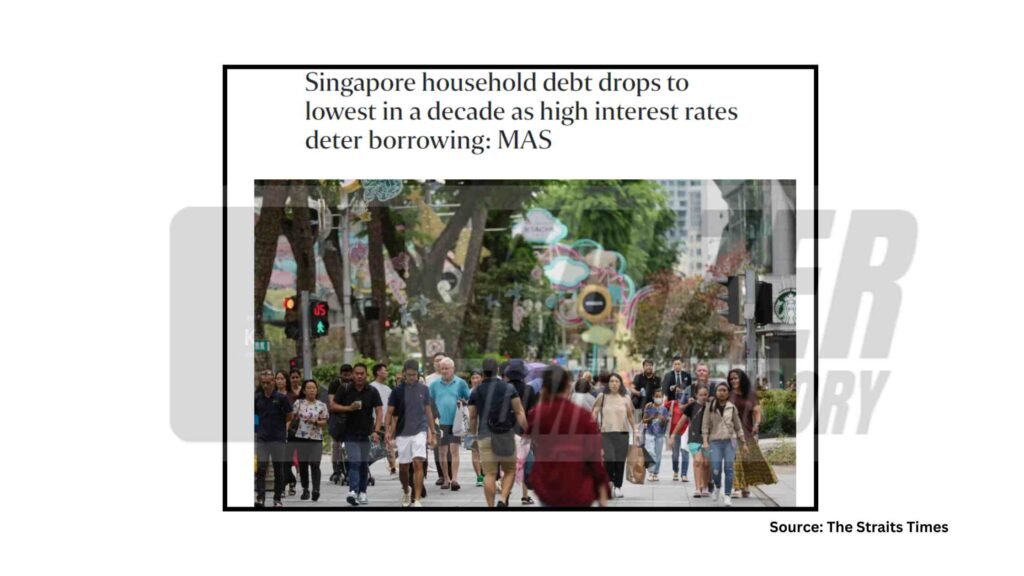

3. Lower household debt

The Monetary Authority of Singapore (MAS) reported that Singaporean households have decreased their debt levels to 1.2 times personal disposable income, the lowest in over a decade, due to high interest rates and healthy income growth. (Read More)

Increased stress tests from all the banks also led to smaller loan size as discussed above.

Since home owners are bearing a lighter mortgage with growing income, what are the chances of them defaulting the loan? Probably it is slim to none.

As long as home owners are financially healthy with no urgency to offload, do you think Singapore property prices will drop or remain firm?

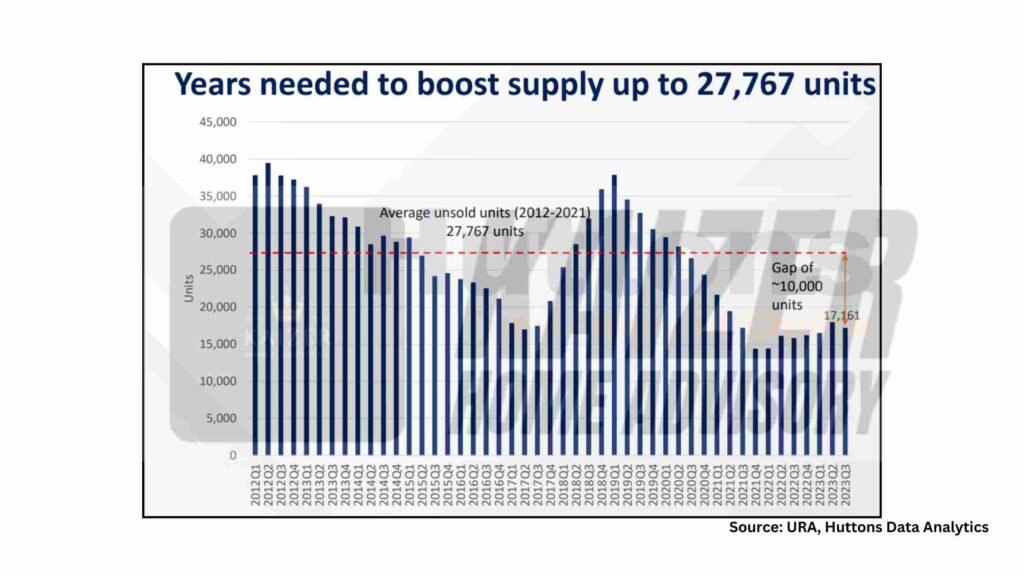

4. The current supply

We often hear property agents say the demand is through the roof but supply is not enough in the market.

What exactly does it mean?

According to URA data, from 2012 to 2023, the inventory of new private homes varies each quarter, with some being high and some low.

The red dotted line represents the 10-year average inventory (which you can also understand as the balance state for stable prices), with a number of 27,767.

As of the third quarter of 2023, the inventory of new private homes is 17,161. This is about a 10,000 unit difference.

What does a 10,000 unit difference mean?

Simply put, it indicates a supply-demand mismatch: High purchase rates causing the remaining stocks levels to be low.

Back to basic: when the supply is lower than demand, will property prices drop or go up?

What Your Goal And Needs?

First and foremost, you must clarify the purpose of your purchase. Are you buying for personal use or for investment?

Family occupation

For own-occupation, if you can fulfill these three criteria, now is a good time to buy.

- You have a very urgent reason: such as not being able to get married without a house, or your children growing up and needing their own rooms.

- You found a once-in-a-lifetime house: This house is one of a kind, checks all the boxes, and you absolutely love every attribute of the house.

- The mortgage is one-third of your monthly income: Everyone has other expenses beyond their home loan, so capping it at 30% of your income will be relatively safe.

If you checked all three, your purpose for buying a house is not whether the house price will rise or make profit, but rather you have specific issues that need to be resolved.

Investment driven

If your family’s financial is healthy and you got some funds to buy a property for investment, then finding the right and safe entry price is paramount.

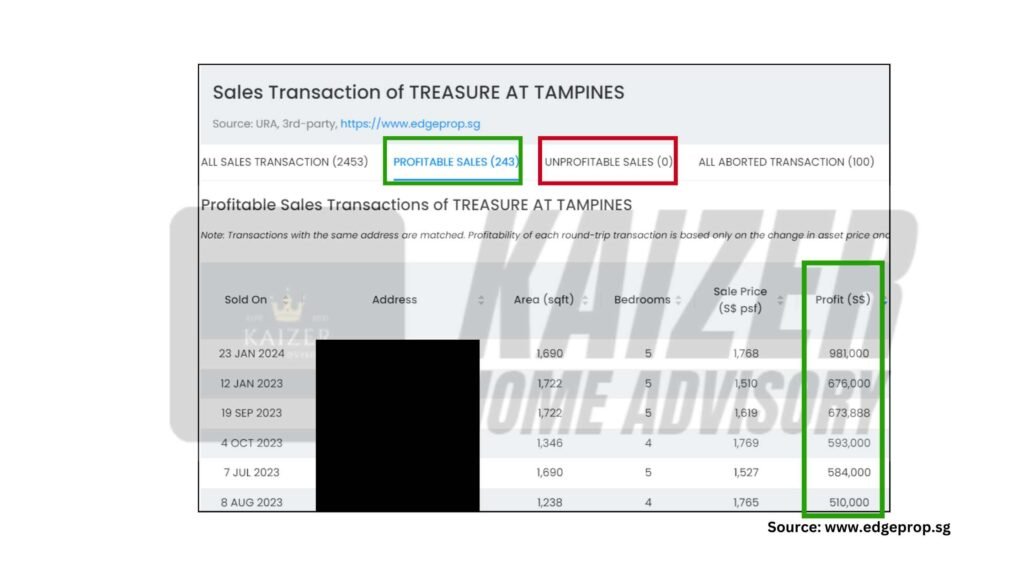

Take a look at one of the recently TOP project, Treasure At Tampines

Entering at a safe entry prices will easily make you a 6-figure profits if done right.

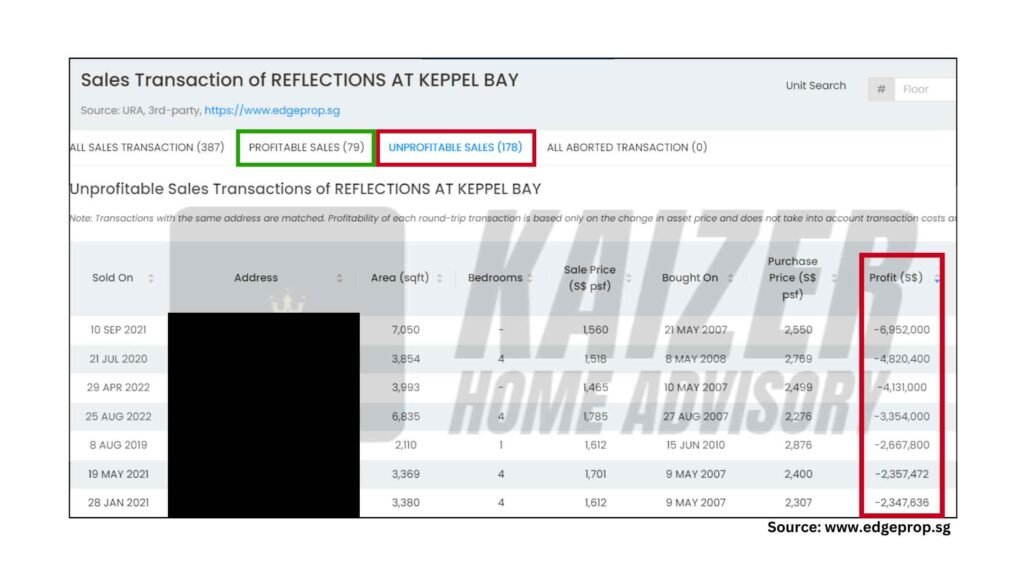

Invest into a new launch condo does not guarantee you “confirm make money”.

The outcome of entering at a wrong entry prices is catastrophic. Many owners chose to offload with even a 7-figure losses.

If you have a choice, which side would you pick?

So Should I Buy Or Wait?

After reading till this point, should you buy or wait? I say no one can accurately time the market.

It entirely depends on your personal and current family situation. There is no right or wrong, only what is or isn’t suitable for you.

As long as you’ve met the criteria above and financially fit, go ahead and buy now if you find the right home for your family.

On the flip side, if you pick the latter, understand that mortgage rates maybe high now but you can always refinance later when the rate cuts arrive.

When rate cuts happen, more buyers will come back into the market, prices will start flying again.

No one wants to pay more for the same item or product, right?

Contact Me

To buy a house now, you might feel pressured and overwhelmed but waiting too long can present challenges as well such as shorten loan-tenure as you age.

Unsure of what to do next? Hit me up, I look forward to work with you.