Skip to content

Skip to content

For many Singaporeans, upgrading from HDB to condo has always been an essential pursuit at certain points in their lives.

One of the motivation for this aspiration is the sense of pride and the elevation of one’s social status it brings. Let’s be frank here: when you start making some papers, you want your family to enjoy a better lifestyle – fancier facilities, 24hrs security and exclusivity.

In addition, other reasons could be relocating near to children’s school or workplace for greater accessibility and convenience.

It’s safe to say that private condominiums emits unique charm that captivates many. That being said, I think it’s important to first weigh the pros and cons before making the leap, so at least you know what you are signing up for.

5 Pros of Upgrading From HDB To Condo

Let’s get into the exciting segment of moving into a private condominium! Here are the 5 major benefits you will get:

1. Exclusive amenities

Straight up – As a condo owner, your family get to enjoy all the exclusive amenities such as the swimming pool, tennis court, BBQ pits and a gym studio, features usually not found in a standard HDB flat.

Some mega project like D’Leedon, located in the prime district 10, offers up to 16 facilities to all its residents. They even have retails shop like coffee house, restaurant and supermarket that you don’t usually see in a normal condo project.

You’d be appreciating these in house facilities on the days where you don’t feel like going out, especially on the weekends where the human and car traffics are high.

Imagine taking the dog out for a stroll; teaching your kids how to swim or chilling over at the clubhouse can all be done within your condo.

2. Privacy & 24 hours security

Living in a condominium covers your family’s safety with security officers working 24/7. Stationed at the guardhouse, they monitor each visitor and conduct hourly patrols throughout the premises.

To a large extent, you will feel safer letting your children go down to the playground without company because they are being monitored and protected at all times.

Another point worth noting is the accessibility and privacy aspect of living in a condo. For your knowledge, only the residents who hold an access card can enter condo and use the lift. This denies all uninvited strangers to infiltrate into your home ground.

Previously when you lived in an HDB flat, I bet you have encountered countless annoying door-knocking salesman, or people asking for charity donation. Sometimes it gets pretty frustrating but all that are beyond your control, right?

Guess what now? You are saved from all the nuisance and unwelcomed guest by living in a condo.

3. Free from HDB rules: MOP, income ceiling, ethnic quota

Whether you are buying a BTO or a resale flat, you are subjected to a bunch of restrictions from HDB.

Why? Because when buying an HDB flat, you will receive substantial helps from the Government in the form of grants and subsidies. (Read More)

In all fairness, you gained something but at the same time you are being “handcuffed” to something as well.

The most widely known rules are:

- Minimum Occupation Period (MOP): 5 years for standard flats whilst 10 for plus and prime model flats.

- Income Ceiling: Combined income not exceeding $14,000 for BTO flats, plus and prime flats.

- Ethnic Quota: To promote balance mix of different ethnic groups within the block and estate.

As a private condo owners, you are not bounded by the above restrictions at all.

Without MOP, you can instantly rent out your unit to a tenant and start collecting rental income. You can also, sell your condo anytime but take note you will be liable to pay the Seller Stamp Duty (SSD) if you choose to offload with less than 3 years of holding.

Secondly, the income level does not matter much, anyone who is financially healthy are welcomed to buy a condo.

Lastly, you can sell your private condo to a much wider pool of potential buyers including foreigners without any hurdles. Unlike in a HDB flat, where most transactions can only occur between the same ethnic group.

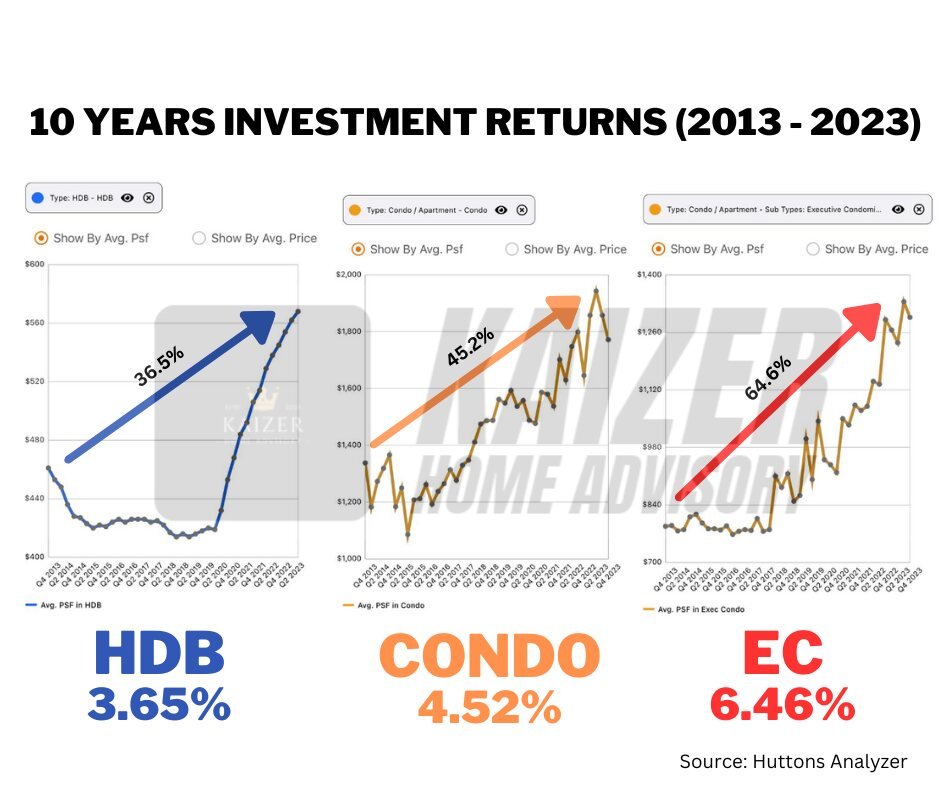

4. Asset Progression

You “sort of” know or probably heard from friends that upgrading to condo or EC can make money.

In reality, HDB can make money too. But the question is – how much?

Let’s do some assumption – Both are appreciating at the above rate (HDB: 3.65%, Condo: 4.52%)

| 2024 | 2025 | 2026 | 2027 | 2028 | |

|---|---|---|---|---|---|

| HDB – $600k | $621,900 | $644,599 | $668,127 | $692,513 | $717,790 |

| Condo – $1.5m | $1,567,800 | $1,638,664 | $1,712,732 | $1,790,147 | $1,871,062 |

After 5 years, HDB would have a paper profit of ($717,790 – $600,000) = $117,790

After 5 years, condo would have a paper profit of ($1,871,062 – $1,500,000) = $371,062

Simply by owning a condo, the owner could potentially experience 3 times more in appreciation in 5 years time than owning a HDB flat.

Hypothetically say your partner is sick, you can choose to ride a bicycle, which takes about 45 minutes, or drive a car, which only takes about 10 minutes, to get to the hospital.

Now, both vehicles can get you to the destination but when time is running out, which would you pick?

Remember time can be your best friend, or your worst enemy.

5. Able to extract equity out

This is also known as the “Equity Home Loan”, or cash out refinancing. It allows you to extract the equity you have built up in the property, without having to sell it.

For HDB flat owners, you are prohibited from doing this, and it is only available to the private property owners.

A simple example would be, say your current condo is valued at $1.5million with an outstanding loan of $800k. The amount of equity home loan could be: (75% of $1.5m) – $800,000 = $325,000

With this sum of money, some people can then use it for their children’s oversea education fee, or other business related costs.

5 Cons Of Upgrading From HDB To Condo

Obviously, there are 2 sides to a coin and we should not overlook on the potential downfalls when you are upgrading from HDB to condo.

So here are the 5 less-talk-about cons you should take note of:

1. Higher cash outlay

To buy a resale HDB flat of $500,000, the initial cash needed is $5000. (Option + exercise fee).

In contrast, to buy a resale condo of $1.5m, you would need to prepare $119,600 as your initial cash outlay:

- 1% Option Fee = $15,000

- 4% Exercise Fee = $60,000

- 5% Buyer Stamp Duty = $44,600

Please take note for condo purchase the down payment is 25% + BSD , 5% in cash, 20% in cash/CPF monies. Hypothetically say you don’t have enough CPF monies, you will be required to top up the shortfall in cash.

So in the worst case scenario, you will need to prepare $494,600, closed to half a million just for the down payment.

This is definitely not a small amount whereby an ordinary Singaporean family can effortlessly pull out from their back pocket!

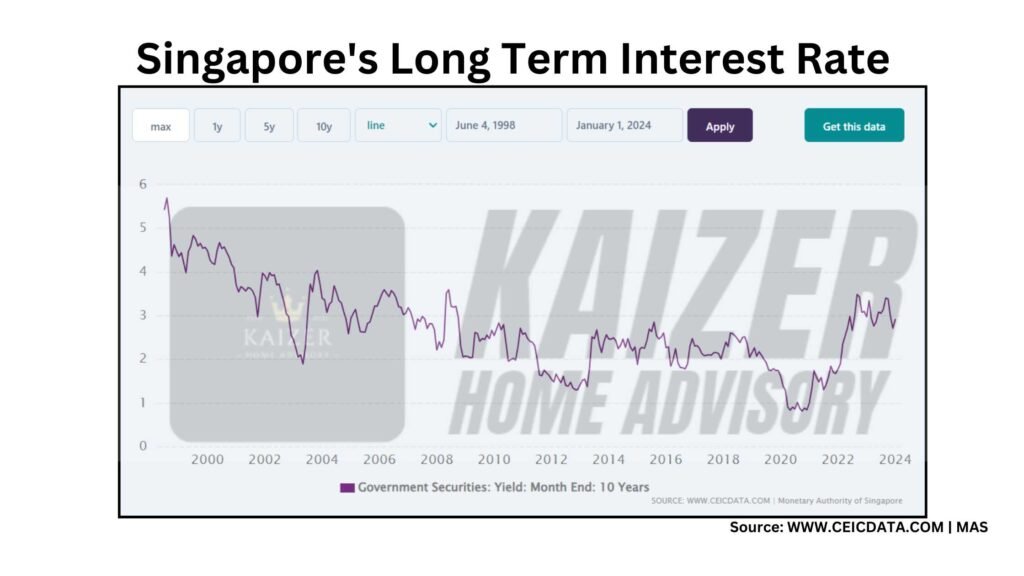

2. No more HDB loan, only bank loan; higher MI

One big perk for an HDB flat owner is being able to enjoy the affordable HDB loan at fixed rates of 2.6%. (pegged at 0.1% above CPF Ordinary Account interest rate of 2.5%).

This rate has not changed for the past 20 years or so.

However, things are a lot different when you upgrade to a private home. Now you can no longer use a HDB loan to service your private home loan, only bank loan.

As we can see, the bank interest rates fluctuates a lot, it can be as low as 1% in 2020 and hovering around at 3% at the time of writing.

Take an example of a loan amount of $1m, 25 years at 1%, the monthly installment would be $3,768. And at 3%, it is now $4,742.

That’s an extra $1000 atop your normal amount!

Worst still, if you do not have any spare funds for rainy days, this sudden increment in mortgage will likely suffocate you.

3. Smaller floor space

People always say condos are smaller than HDB, to some degree, they are right.

So how much smaller are we talking about here?

Above is a comparison of a family-sized 3 bedroom unit between HDB and condo. There is a clear difference of 17sqm or 182sqf in terms of the overall floor space.

Also, take a look at the price tag – the price of a typical 4 room HDB flat is around $600,000 whereas a brand new 3 bedder from Lentor Mansion (Latest New Launch in 2024) comes with a price tag of starting from $1.7xm.

Theoretically, the price you pay for the condo is easily 3 times more expensive than a normal HDB flat.

4. Higher Maintenance fee

For HDB owners, you do pay HDB maintenance fees which also known as the Service & Conservancy Charges (S&CC).

This money goes to the different town councils for maintain the HDB estate.

Depending on your HDB flat type, the S&CC fee range from $20 to $101 for Singaporean household. The bigger your flat is, the more you pay.

In January 2024, all eligible HDB owners will receive S&CC and U-Save rebate given by the government, which can be used to offset the utility bills.

Similarly, private condo owners have to pay maintenance fee too, to maintain the amenities, landscaping and security guards of your home ground.

How much to pay? It is somewhat the same, the bigger your unit is, the higher share value you hold, the more you pay. Do take note if you live in a boutique condo with lesser unit, your maintenance fees will be higher than normal as there are fewer owners contributing to the fund.

The main different here is though, you do not have any form of subsidy nor rebates from the government because you own a private property.

There have been cases (Dairy Farm Residences and Parc Komo) where owners were shocked and upset about the absurd rise on condo maintenance fees.

So, prepare mentally to pay higher maintenance fees and expect “surprises” if you decide to upgrade to a condo.

5. Unable to transition back to HDB immediately

Buying is always the easiest part. Put down the 25% down payment plus stamp fees and there you go! You are now officially a private property owner!

But let me ask you this: Have you ever heard from the “Buyer’s remorse”?

It happens when you buy something on impulse and for the moment of excitement, afterwards you start feeling regretful about it.

In this situation you could still sell off your condo immediately due to “Buyer’s remorse”.

However two things to note:

- You will be liable to pay the 12% Seller Stamp Duty (SSD) for offloading in the first year of purchase.

- You have to wait 15 months before you are allowed to buy a resale flat from the open market if you are below 55 years old. 30 months if you wish to buy a BTO flat.

Or it could be one of you suddenly experience loss of income due to illness or retrenchment and you are unable to saddle the hefty monthly installment of your condo.

The same applies, you could sell instantly, but SSD will be payable and cannot buy a HDB flat immediately.

If you ever go into that predicament, the only option left for you is to rent a place or move back to your parent’s place.

Should You Still Be Upgrading From HDB To Condo?

Now you should have a clearer view on the big picture before progressing to a condo. There are alluring rewards and terrifying risks await you for making the leap.

Ultimately, most of challenges are dealing with money – higher cash outlay, higher price tag (in terms of PSF), higher monthly home loan, higher maintenance fees, higher risk of “being homeless”.

I would say, do your math right, ensure your financials are healthy, keep a sum of emergency funds for rainy days and lastly, never over-stretch on your budget! Always purchase within your mean!

That way, you will easily overcome these potential hurdles in your home upgrading adventure!

Contact Me

Thanks for reading till this point!

If you are thinking of upgrading from HDB to condo, do check out this blog post to learn more.

For a more personalized discussion, feel free to reach out to me via any of my social media platform!