Skip to content

Skip to content

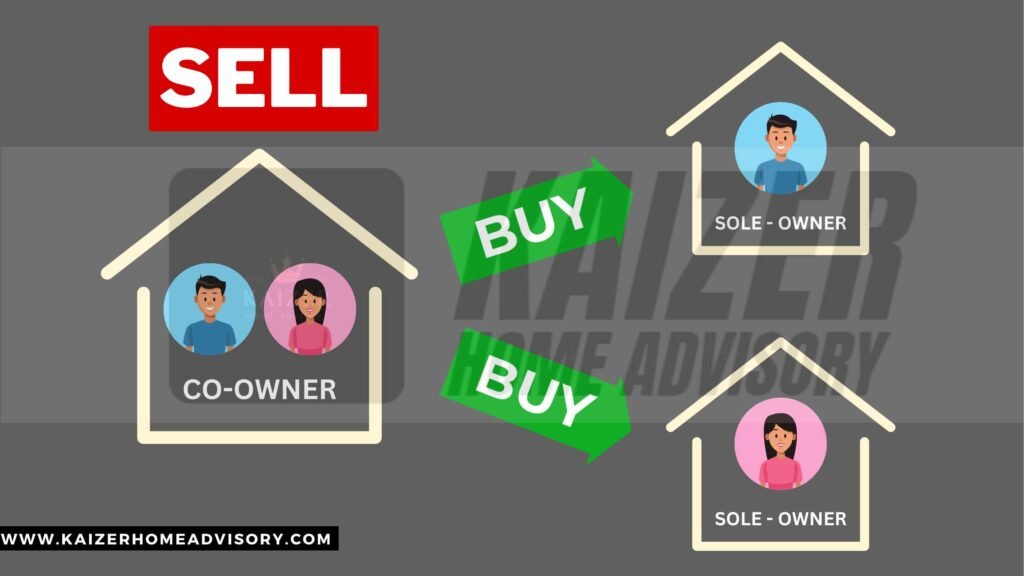

The “Sell One, Buy Two” method needs no introduction for those who have been in the property market for awhile. Some of you may have seen it online, heard from an agent or perhaps successfully done it in the past.

People who knows very little about the strategy of selling one HDB and buy two private properties might be wondering, “How does it work? Achievable? Safe or not?”

It is indeed a popular method to own two condos without incurring ABSD.

Understand that it is not for everyone though, good things do come with risks.

To clear all your doubts, this article will give you full insights on how it works, the logics behind it and the risks involved.

How Does “Sell One, Buy Two” Work?

The secret is to leverage on the sales proceeds from selling your HDB or EC, to buy 2 private condos.

Ideally, the method advocates buying a family-sized unit for own occupation, and another smaller unit for investment (to be rented out), under each spouse’s name respectively.

Subsequently offsetting its monthly mortgage from the rental income and using the excess cash flow to further cover the mortgage of the own-stay home.

In order for this strategy to work, it requires the combination of the cash proceeds unlocked from the co-owned home, CPF monies, rental income and savings from your piggy bank.

Why is “Sell One, Buy Two” so popular?

It was a strategy created to combat HDB disallowing ownership transfer among HDB flat owners back in 2016. (Read More)

Simply put, HDB owners could no longer transfer his/her shares to the spouse and buy a second private property without paying ABSD.

Moreover, the Additional Buyer Stamp Duty (ABSD) adjusted from 12% to 17% back in December 2021 for Singaporeans buying a second property, followed by further revision from 17% to 20% in April 2023.

This method soon gained massive attention among property owners as the two properties are owned by each name, and neither party has to pay ABSD as such.

Examples of “Sell One, Buy Two”

1. “Sell One HDB”

For simplicity sake, let’s assume the couple is going to sell their fully paid HDB flat worth $680,000.

After the sale, the husband will have $340,000 in his CPF Ordinary account and $100,000 cash proceeds. For the wife, she will have $220,000 in her CPF OA account and $100,000 in cash.

Total fund available to buy two condos will be $760,000 combined.

2. “Buy Two Condos”

The recommended way is for the husband to buy a family-sized unit (At least a 3-bedder) for own stay and the wife to buy a 1bedder shoebox condo for rental income.

The total cash portion for 2 condos would be the 5% + buyer stamp duty (to be paid in cash first for resale property), which comes out at $186,200.

| Cash Proceeds | 5% in Cash | Stamp Duty | Balance | |

|---|---|---|---|---|

| Husband | $100,000 | -$75,000 | -$44,600 | -$19,600 |

| Wife | $100,000 | -$45,000 | -$21,600 | $33,400 |

| Total | $200,000 | -$120,000 | -$66,200 | $13,800 |

The couple has $200,000 in cash proceeds from the sale of their HDB flat, which is just sufficient to cover the 5% cash portion + stamp fee for the 2 condo purchase., with a mere $13,800 to spare.

On the remaining 20% down payment in CPF,

| CPF OA | 20% Down Payment | Balance | |

|---|---|---|---|

| Husband | $340,000 | -$300,000 | $40,000 |

| Wife | $220,000 | -$180,000 | $40,000 |

| Total | $560,000 | -$480,000 | $80,000 |

The couple will have $40,000 each remaining in their OA after paying off the 20% down payment using their CPF monies.

Reserved Fund/ Safety Net

A quick summary of the balance figures after the couple has successfully paid the 25% down payment + stamp fee:

| CPF OA | Cash | Total | |

|---|---|---|---|

| Husband | $40,000 | 0 | $40,000 |

| Wife | $40,000 | $13,800 | $53,800 |

Assuming the couple is relying on the balance fund to service the monthly loan repayment,

- Husband – $40,000/$5,371 = 7 months

- Wife – $53,800/3,223 = 16 months

The husband will have 7 months worth of safety net to cover the own stay property while the wife’s fund is enough to cover her for 16 months without forking out extra cash.

Rental Income to ease cashflow

As of Q1 2024, the average price is about $6.20psf for 1 bedder condo rental. The expected rental income is roughly between $2800 and $3000.

| Monthly installment | Monthly OA Contribution | Rental Income | Balance | |

|---|---|---|---|---|

| Husband | -$5,371 | +$1,380 | $0 | -$3,991 |

| Wife | -$3,223 | +$1,380 | +$2,800 | +$957 |

| Total | -$8,594 | +$2,760 | +$2,800 | -$3,034 |

Assuming the couple is making $7000 each and have incoming OA contribution every month, plus the bonus rental income, the final cash top up will be $3,034 for owning 2 private condos.

5 Potential Risks Involved In “Sell One, Buy Two”

Only cost $3,034 to own 2 private condos! Sounds workable right?

Hold your horses, let’s dive into the potential risks you might overlook when considering doing the same.

1. Age & income level

The above example we assumed the couple was able to qualify for the max loan of 75%, tenure 30 years at 4% interest rate.

What if you are older and have shorter loan tenure?

| Husband, Max loan of $1.125m | Wife, Max loan of $675k | |

|---|---|---|

| 50 years old | $15,129 | $9,076 |

| 45 years old | $12,395 | $7,436 |

| 40 years old | $10,769 | $6,476 |

| 35 years old | $9,763 | $5,858 |

The above table depicted the MINIMUM INCOME for the couple in order to qualify for the max loan amount at different age.

To qualify for the same loan amount at an older age, you have to be earning much higher than you were younger!

These numbers are derived from the TDSR of 55%, excluding of any car loans and credit card loans.

So, if you do own a car (most people do) and have an existing car loan, or bad credit scores, my dear friend, the income level required from you will be way HIGHER than this.

Simply put, if you can’t meet the minimum income level, you can’t get the full loan. Without enough loan, this method can’t work.

2. Unspoken fee

Other less-mentioned expenses such as

- Maintenance fee (Depending on share value, bigger unit = higher share value)

- Property tax (Higher for non-owner occupied property)

- Income tax (Rental income is taxable)

- Agent fees (If you engage one)

- Renovation cost (Ranging from $80k – $120k)

These less-talk-about fees EXIST and they do add up on top of your monthly installment.

3. Risk of unit vacancy; bad tenants

Multiple mega projects in 2023 received TOP, roughly 20,000 units were poured into the market.

The supply avalanche forced many landlords to lower their asking rent to avoid prolonged unit vacancy.

As a landlord, you are literally losing money the moment your unit is untenanted.

Also, being a landlord, sometimes you ought to encounter late payment from tenants, in some of the worst scenario, you might even have to go to the Court to evict the over-staying tenants who refuse to leave nor pay you.

4. Exit strategy

The level of difficulty in offloading your condo to the next buyer is paramount.

Imagine running into unforeseen financial hard times or cashflow problem, you urgently need to offload, how quickly can you do that?

The demand for a resale 3-bedder family-sized unit is always healthy as there will always be family- upgraders, so selling it to the next buyer is not difficult.

Conversely, owning a 1 bedroom condo might be a problem. Why? It is so saturated as there are so much supply of shoebox units on the resale and new launch market.

What is the likelihood of people buying from you when there are plenty of options out there?

5. Unexpected income loss

“Sell One, Buy Two” also imply that each owner saddles the home loan individually.

Hypothetically say, one day you received a surprise letter from your boss informing you: “Dear Mr. Sam, your current position as GM will be demoted to Assistant Manager with immediate effect…”

Guess what gets demoted too? Yes, your salary.

These unpredictable events lead to decreased income and instantly put you in a cash-flow crisis.

Is “Sell One, Buy Two” Suitable For You?

In a nutshell, “Sell One, Buy Two” can still work but it is not everyone.

It is suitable for the more affluent Singaporeans with higher risk capacity.

People who are in a better financial position and own a higher value home such as EC owners, who are sitting a bigger profits margin will likely have a lower risks compared to HDB owners doing the same strategy.

End of the day, each owner has to bear the entire loan on their own, it can be frightening and challenging.

I highly recommend to people who wish to own a private condo to do a simple upgrade; upgrading to a bigger home and share the home loan equally. This way the burden will be much lighter.

Still keen? Reach out to me for a discussion.