Skip to content

Skip to content

“Buy Condo confirm make money one!”

You’ve probably heard from plenty of relatives and friends around you, or seen online, the claim that “upgrading from HDB to condo can easily make you S$250,000 to S$400,000 in just 3 to 4 years.”

The truth is, this mantra is quite prevalent in the local property market scene.

Most Singaporeans start with a HDB flat and, after fulfilling the 5 years MOP, sell it to cash out and use the profits to upgrade to a private condo.

Nonetheless, in the face of heightened macroeconomic uncertainty, elevated interest rates, and the implementation of various cooling measures, most are mulling over whether is it still feasible for HDB flat owners upgrading to a private condo in 2024?

Let’s dive into what’s going on in Singapore’s property scene and see if this move makes sense for you.

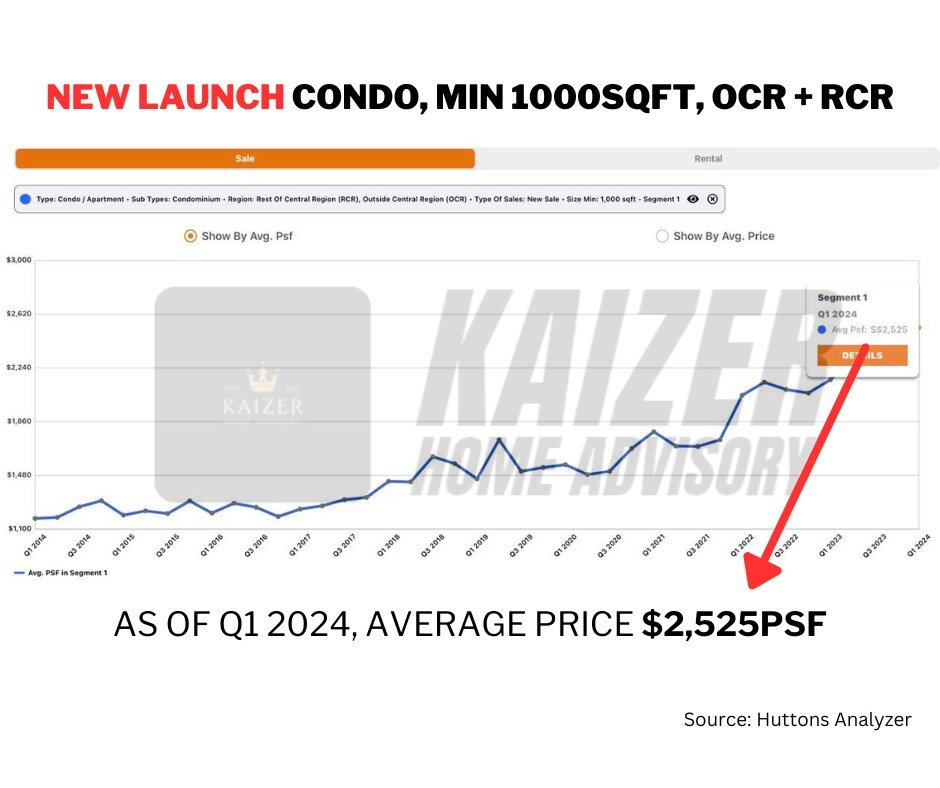

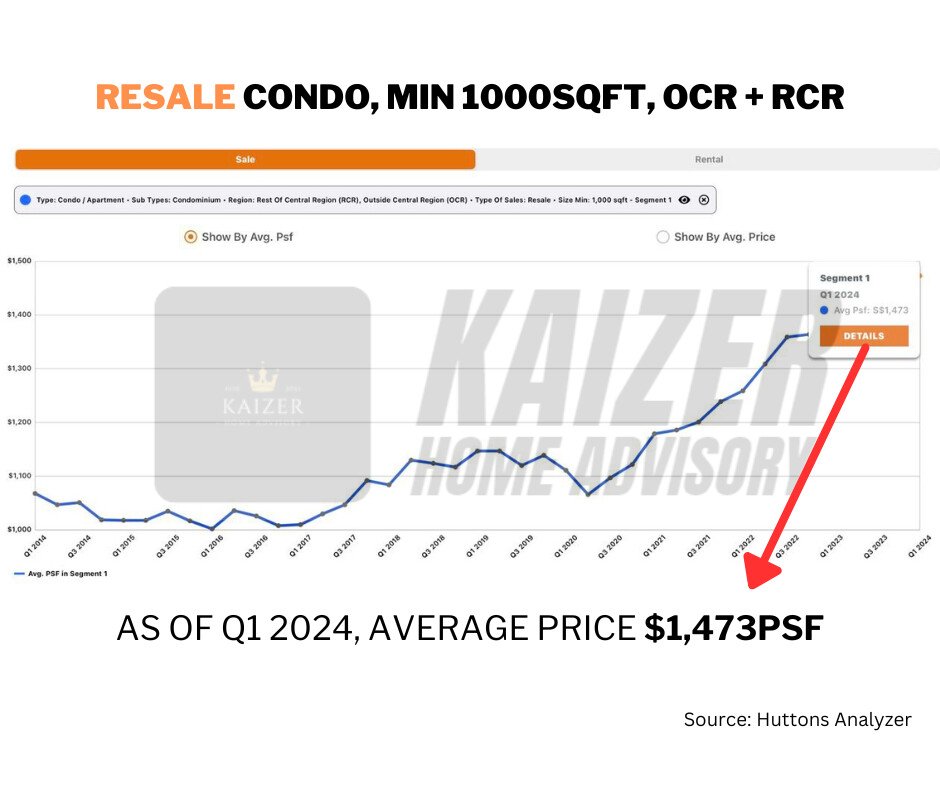

Condo prices in 2024

First of all, let us look at the price trend as of 2024,

The above two graphs are pretty self-explanatory, both illustrated the current average price you can expect when buying a non-landed private condo unit in 2024.

The key points to note here are the filtering criteria to OCR (Outside Central Region) and RCR (Rest of Central Region) areas, as well as units over 1000 square feet. There are two reasons for this:

First, most HDB flats are located in the OCR and RCR regions. Therefore, when HDB owners want to upgrade, they often choose to buy their new homes in the same or nearby suburbs. Compared to the premium prices in the central region, the OCR & RCR areas are more attractive in terms of price, making them the preferred choice for HDB upgraders.

Second, most HDB upgraders are usually families of 3 to 4, so “upgrading” to a 1 or 2 bedder shoebox condo will not make sense at all.

Especially if their previous HDB flat was around 900 to 1000sqft. Therefore, when people are upgrading from HDB to condo, they also tend to buy units that are roughly the same size or bigger, to accommodate the whole family.

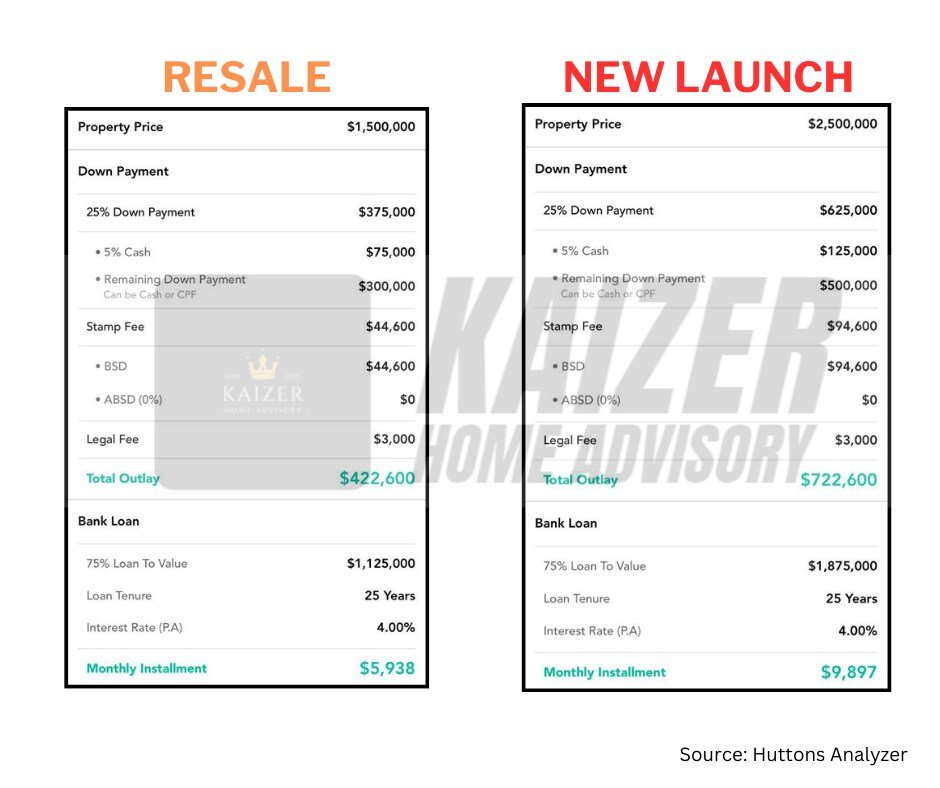

How much do condos cost?

Using the example price tag from above, for a 3 bedder new launch condo with minimum size of 1000sqft, we are looking at quantum of around $2.5m, and resale condo at around $1.5m in the suburbs regions.

Let’s see the breakdown of the cost involved:

Total down payment for a new launch condo will be $722,600, monthly installment of $9,897.

Total down payment for a resale condo will be $422,600, monthly installment of $5,938.

affordability vs over-stretching?

Before we move further, let’s understand more about your individual affordability. Straight up, if your financial capability does not cross the line, forget about upgrading. You have to know, once you make the jump from a HDB to a private property, there is no turning back.

Meaning, one can’t just simply transition from a private property back to a HDB flat no matter what. There is a 15 month wait-out period rule implemented for private property owners who are below than 55 years old, disposing their private home before they can buy another resale HDB flat. (30 months applies if buying a BTO).

As you can see, the consequence is brutal. If you ever fall into that predicament, the options left for you are to either move back to your parent’s place or rent a temporary place till the ban period is over.

can hdb upgraders afford a condo?

Coming back, let’s talk about the Total Debt Servicing Ratios which, limits the monthly debt obligation to 55% of your gross income, including car loan, student loan and credit card loan. Nonetheless, the more prudent way, in my opinion, is to keep your monthly mortgage at around 25% – 30% of your gross earning. (Nobody whack until max one lah!)

Therefore, in order to qualify for the full loan, your combined household monthly income has to be at least:

- New Launch Condo: ($9897/0.55) = $18,000 (Rounded up)

- Resale Condo: ($5938/0.55) = $10,800 (Rounded up)

Assuming you and your spouse have fulfilled the minimum income level, next thing we are going to discuss on, will be the down payment portion.

Let’s be real here, most people have their funds locked in their current HDB flat, and the only way to unlock their capital is by selling off, coupled with their savings from past recent years, to hit that figure. Without selling off your current flat, upgrading is just another dream.

Hypothetically say, if you own a typical 4-room HDB flat worth around $600,000, after deducting the outstanding loan, you will likely have sufficient down payment to upgrade to a resale condo; for those who owned a higher value flats worth over $850,000 in the prime estate, e.g. Bukit Merah/Queenstown/Bishan, the sale proceeds will be enough to go for a new launch condo.

On the other hand, if you own something that is below $500,000 and does not have much savings, then your property upgrading journey will be vastly different from what I have covered above.

Everyone’s situation is unique and complex, feel free to reach out to me for a more personalized breakdown and proposal tailor to your family’s needs.

Should you upgrade or remain status quo in 2024?

After careful assessment on your overall financial health, you might find yourself in a good position to upgrade, but the macroeconomies uncertainty is high, interest rates are at all time high, borrowing costs are much higher than before. You are unsure whether is it worth the cost to move forward or just stay put?

Below are some factors we have to take into consideration before making a decision:

- Price gap between HDB and private home

- Investment returns for the past 10 years

- Future demand & upcoming supply

- Interest rates movement

- Upgrading lifestyle or net worth

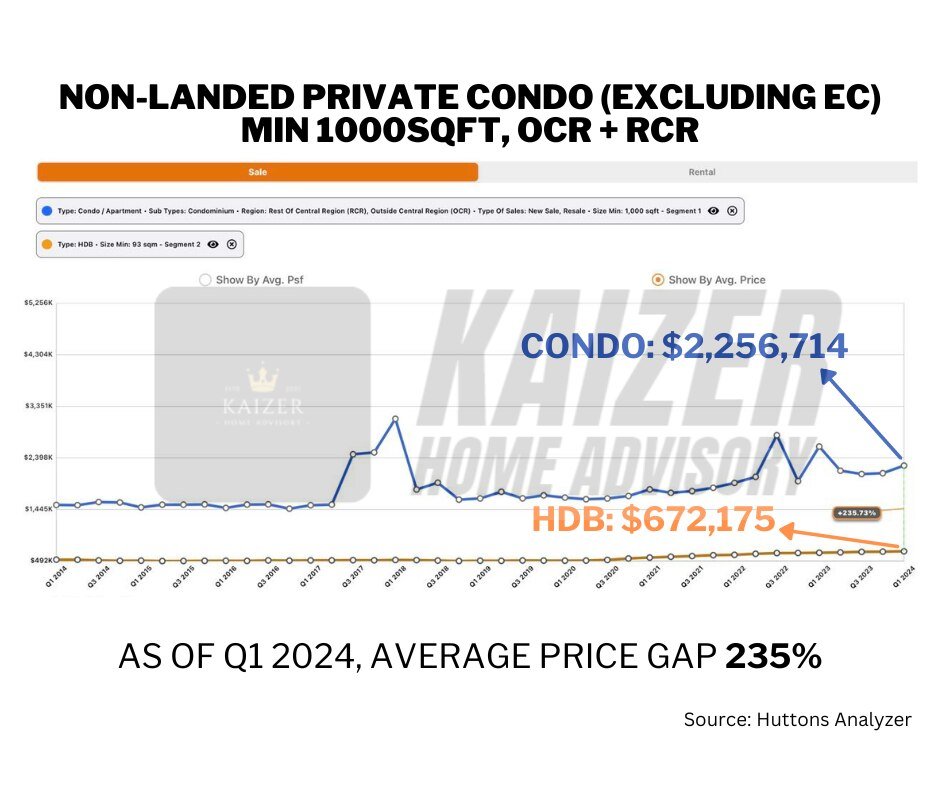

Price gap between HDB and private home

Despite HDB resale prices reaching all-time high in 2023, the gap between the two is still pretty substantial and often seems far from reach for the average home buyers.

One of the reasons come from the ever rising land cost, raw material costs and labor costs for the private developers, which will eventually translate to higher price tag to the end consumers. Whilst, HDB flats are heavily subsidized by the Government to ensure it remains affordable to Singaporeans.

In other words, HDB’s price growth are limited and controlled by the Government while private homes have lesser restrictions, presented a bigger room for appreciation.

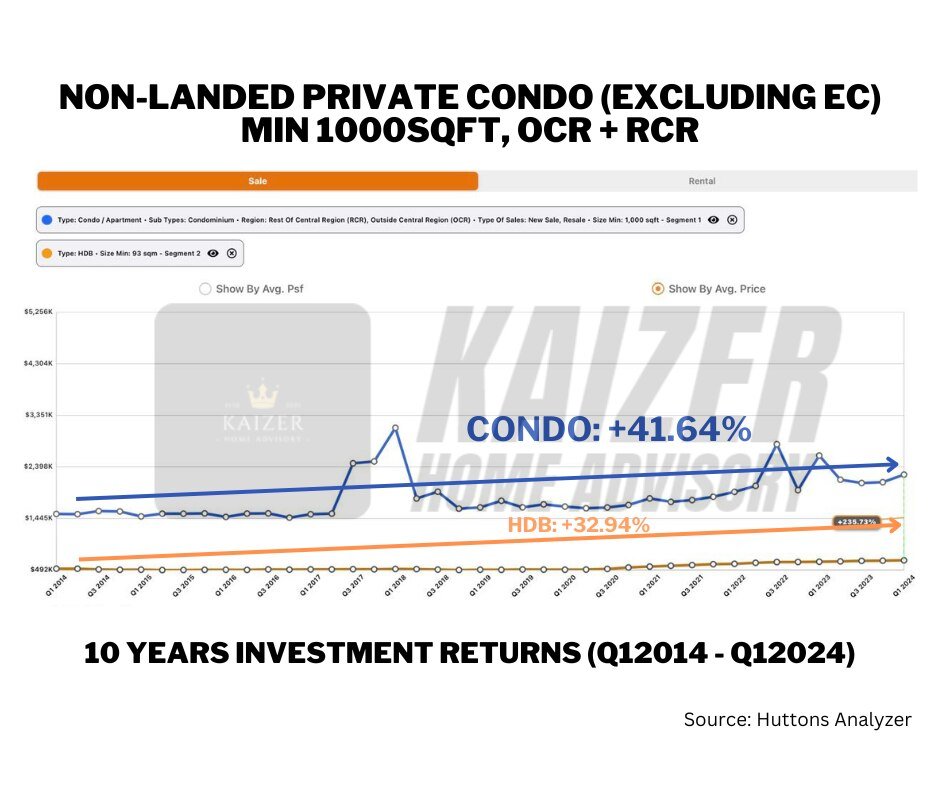

Investment returns for the past 10 years

Owning and staying in a HDB flat with a 3.3% growth isn’t too bad after all, given its low entry price and affordability. But hey, do you know what was past inflation rate in SG?

As of 2024, Singapore’s inflation rate is projected to be at around 3.1% to 3.4%, albeit a dip from 5% in 2023.

I strongly believe if you ain’t growing, you are effectively losing out, in terms of benefits relative to inflation.

In the context of property investment, this implies the opportunity cost associated with idle or stagnated assets. Money that is not invested could be losing value over time due to inflation. In a broader sense, it is important to stay proactive in upgrading your assets, rather than remaining passive.

End of the day, does anybody gets upset for picking the winning side? Well, not me, at least.

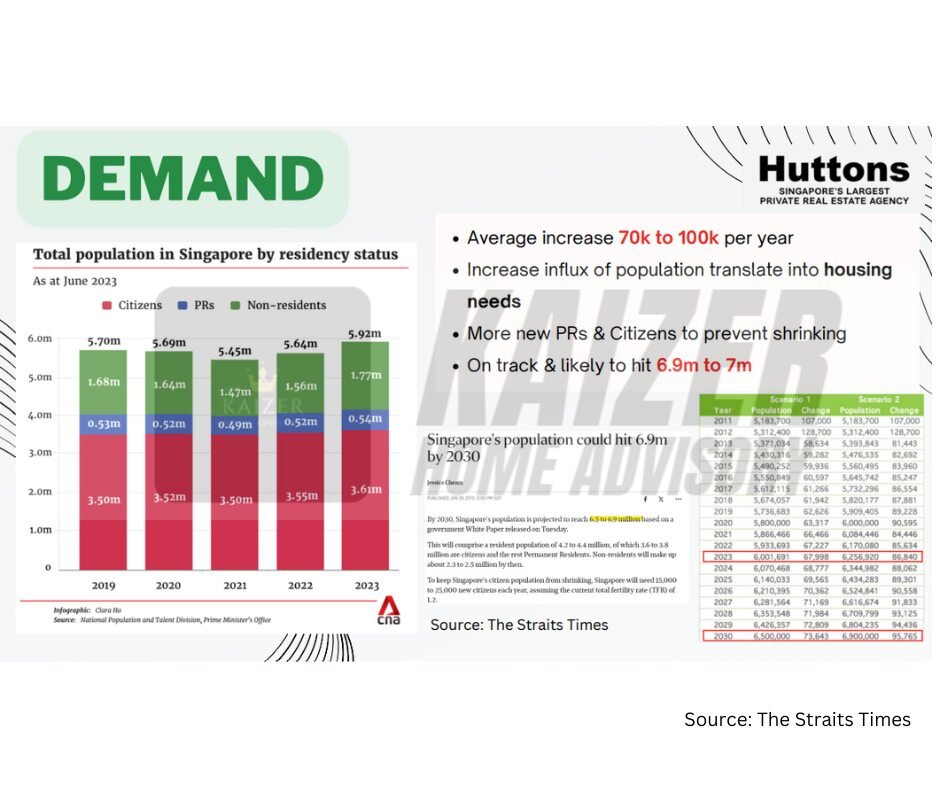

Future demand & upcoming supply

The current HDB price index is at all-time high from 2021 till present. But will it last? (Graph 4.3.1)

Property prices fluctuates actively based on demand and supply. Our National Development Minister Desmond Lee has publicly announced the Government’s plan on 100,000 new BTO flats to be injected into the market by 2025. (Graph 4.3.2)

The main goal is to fulfil the pent up demand and prevents HDB prices from sky-rocketing. HDB prices HAVE to remain affordable at all time. (Graph 4.3.2)

Singapore adds around 53,000 new citizens and PR annually over the past 10 year and is growing at around 100k per year. We are on track to hit 6.9million population by 2023. These new citizens and PR will increase housing needs because they can now buy a property without paying additional buyer stamp duty and stop renting. (Graph 4.3.3)

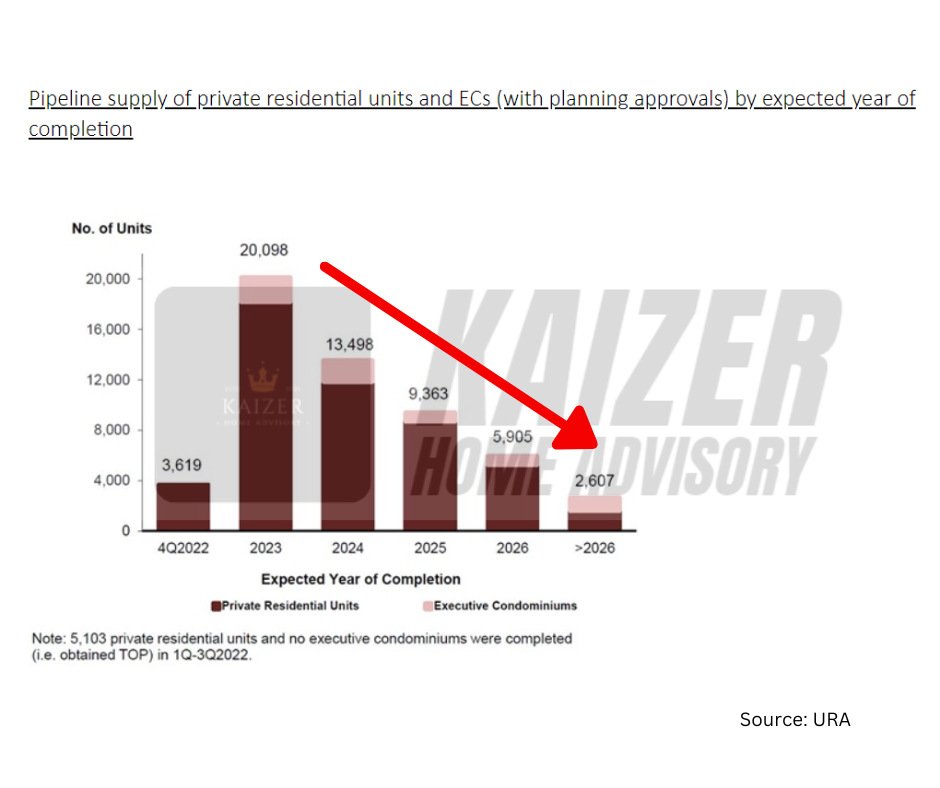

According to URA, the supply of completed private homes will be dipping till 2026 and beyond.

So, with HDB supply avalanche coming its way, do you think HDB prices will go up or down? At the same time, new citizens are adding to housing demand; supply of private home slipping. Do you think private homes price will go up or down?

Interest rates movement

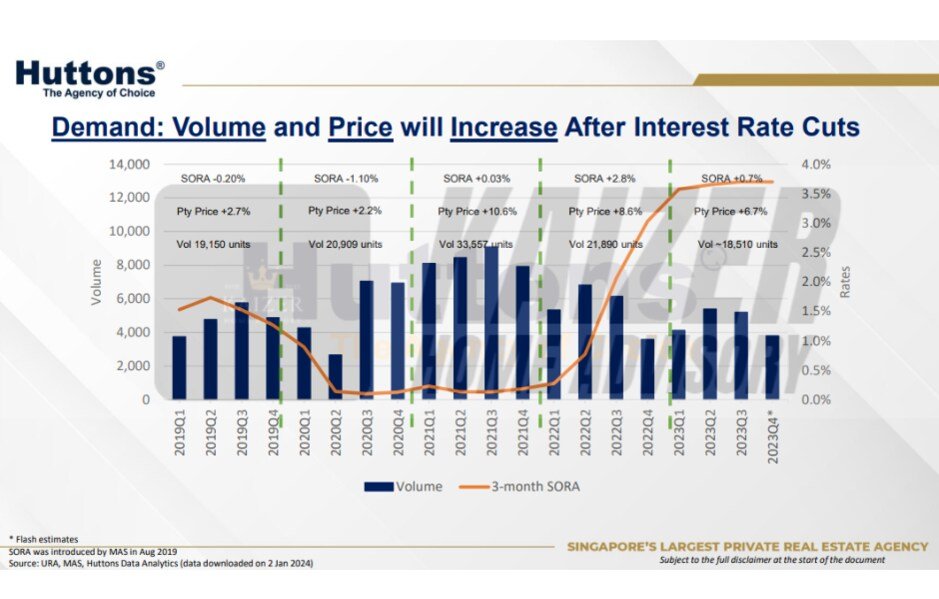

Historically, transaction volume in the property market will spike when there is an interest rate cut. All types of properties from HDB to high-end private non-landed and landed properties will benefit from lower interest rates.

Investors will likely cheer the most. A lower interest rate which may translate into lower mortgage costs makes investing in properties attractive. With a spike in demand, prices may also increase in tandem.

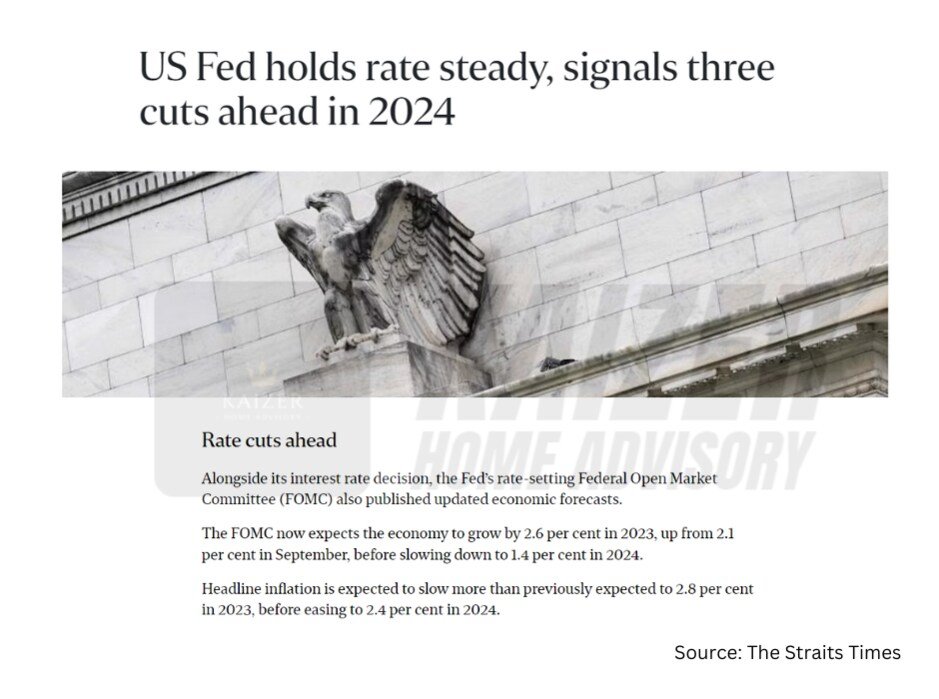

And it was reported in the News, that the Fed signals the possibility of three rate cuts in 2024. Nobody knows whether or not it will actually happen, but here’s the thing:

WHAT IF the rate cuts do happen? Singapore’s local bank rates tends to follow trends set in global money markets, especially that of the US, the world’s largest economy. Meaning, likely the local loan interest rates will also set to stagnate or dip in times to come.

Back then when interest rates were at the 0.5% – 1% range, borrowing costs were real cheap, how about you tell me, what will you do in this situation? Leaving money in the bank or investing your funds elsewhere for better growth?

One question to ponder here, what do you think it is the best time to enter the market? In the uncertain times, everyone is fearful to act despite prices being relatively stable; OR when the market’s confidence level is high, while prices also are HIGH, everyone just rush in to snatch the deal because of fear of missing out?

Upgrading from HDB to condo for lifestyle or net worth

When people consider upgrading from HDB to condo, their motivation can vary widely, often influenced by personal circumstances, financial goals, and lifestyle preferences.

In the end, we need to define what “upgrading” means to you.

Are you upgrading for the luxury lifestyle where you and your family can enjoy premium amenities and exclusive facilities like the swimming pools and gym?

Are you upgrading because of status symbol in your social circles? Owning a private property can be perceived as successful, reflecting a certain level of financial milestone among their peers.

OR it could be, upgrading for the purpose of investment and growing your net worth, leveraging on your property to work hard for you, not the other way around? Most private properties in Singapore often see higher appreciate over time, potentially offering higher returns on investment compared to HDB flats.

FINAL THOUGHTS

Instead of asking is it viable to upgrade, a better question might be: Should you progressively upgrade your net worth through property or continue holding onto a HDB flat?

With that being said, if you are seasoned investor who are super well-versed in different segment of investment like stocks and digital currencies, you have the relevant skills and knowledge to make more returns than investing in private property, then it is not for you.

However, if you are just a regular person, working hard, savings money in the bank, buying basic bonds or savings plan, don’t know about stocks, don’t know how to invest, then upgrading your net worth through property is the way to go.

As upgrading to condo is not for everyone, it requires detailed and personalized planning.

Do reach out to me for the exclusive E-Book: “Using Property to Achieve 7-Figure Net Worth“ to see how it all works and schedule a consultation with me.

I’ll see you soon.